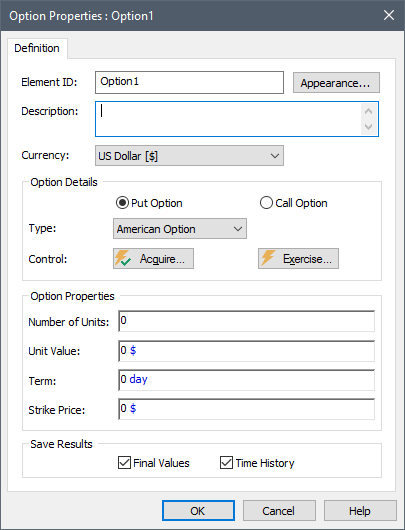

The Option element simulates the acquisition and exercise of financial options (puts and calls).

The property dialog looks like this:

After specifying the currency units you wish to use, you must specify whether you are simulating a put or a call, along with the option type (American European, Asian).

The unit value of the underlying security must also be specified. This can be any function, but will often be the output of a History Generator element. This element (which is part of the basic GoldSim framework), provides a variety of alternatives for generating time histories, including simply specifying a constant annual growth rate, and specifying a stochastic growth rate (defined using a mean annual growth rate and volatility, and simulated as a Wiener process)

Triggers must be specified for acquiring and exercising the option. You must also specify the properties of the option at the time of acquisition (i.e., number of units, term and strike price).

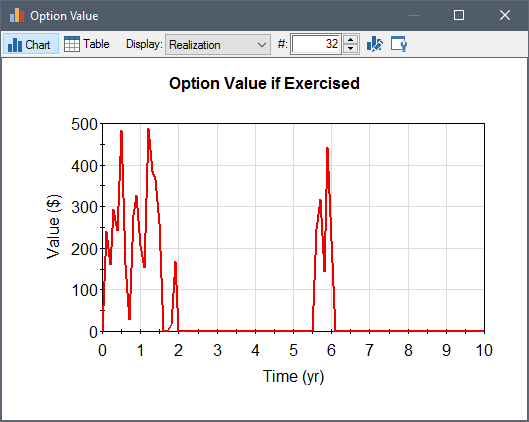

The primary output is current value (if exercised), and a discrete change signal with the value of the exercised options:

Learn more about: